bankruptcy nb

Can I Declare Bankruptcy If I Live Outside of The Country?

Generally speaking, under the Bankruptcy & Insolvency Act, if you reside outside of the country you can still declare bankruptcy as long as you meet certain criteria. If you are a previous Canadian resident and are have debt issues you should contact Powell Associates Ltd. to determine if you meet the criteria to file personal bankruptcy or a consumer proposal in Canada.

Read MoreWill Bankruptcy Take Care of Judgments?

Yes, judgments from creditors do get released when you file a personal bankruptcy or complete a consumer proposal. However, judgments registered against your assets by Canada Revenue Agency do not get released when you file a personal bankruptcy or complete a consumer proposal.

Read MoreUsing RRSPs to Pay Down Debt

If you are unable to keep up with your debt payments you should consult a Licensed Insolvency Trustee to discuss your options before cashing-in any of your investments. Your investment savings may be exempt from seizure so you may be able to keep them if you file for personal bankruptcy or settle your debts through a consumer proposal.

Read MoreBanking Fees – Are You Paying Too Much?

It’s important to find the best type of account and monthly plan to fit your lifestyle so you can start by reviewing your monthly bank statements to see the fees and service charges you have incurred in the past. This will provide the information you need to compare the types of accounts and plans that best suited to your usage.

Having the wrong plan or too many bank accounts can be costly, and you might be paying for unnecessary bank expenses than a plan that is tailored to your individual or family needs.

Read MoreCan Creditors Collect Debts After Bankruptcy?

When you receive a discharge after completing your bankruptcy, it releases you from the debts you owed before your date of bankruptcy. Once you file personal bankruptcy, your creditors cannot legally collect on those debts.

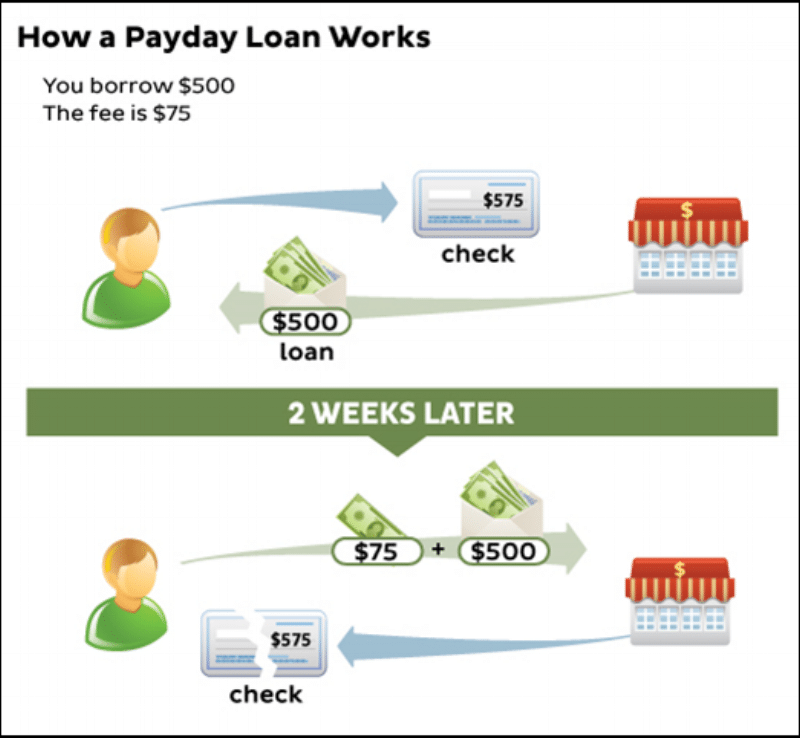

Read MoreCaught in the Pay Day Loan Cycle?

The problem with this type of borrowing is that it is very expensive and can often leave the borrower, who is already in a tight financial position, unable to repay the loan. So they end up re-borrowing or getting a “roll-over” loan by paying off the current loan and immediately getting another one from the payday lender.

Read MorePersonal Bankruptcy and Income Taxes – What You Need to Know

When filing a personal bankruptcy income tax debts are discharged the same as any other unsecured debt, such as credit cards and personal loans. If you are struggling with income tax debt or have had your wages garnished then you should seek the assistance of a professional.

Read MoreGood Debt vs. Bad Debt

Good debt is for purchases that appreciate in value or significantly improve your quality of life. Bad debts on the other hand typically do not provide you with any long-term benefit. If you carry a heavy amount of bad debt and are only able to make minimum payments then it’s time to look for help.

Read More10 Steps To Rebuild Your Credit Rating After Bankruptcy

Once you have been discharged from your personal bankruptcy or consumer proposal there are some steps you can follow to put you on the path to a healthy credit rating.

Read MoreWhat to Know Before Co-signing A Loan?

When you sign for a student loan, line of credit or any type of loan for another person you are legally responsible if that person fails to meet the terms of that credit agreement. If the other person misses payments the creditor will expect you to make the payments and demand that you pay the debt in full.

Read More