Posts Tagged ‘financial stress’

Budgeting 101 – Part 2 of 5

Monthly expenses should be the most predictable of the expense categories. They happen every month. Some are fixed and some are variable. With your household income, you should be able to comfortably cover these expenses including covering seasonal variations.

Read MoreBudgeting 101 – Part 1 of 5

If you want to make a budget, you need to understand your expenses, short-term, medium-term and long-term. Monthly expenses can be fixed or variable. Annual expenses can be fixed and some variable.

Read MoreWill I Lose My Canada Child Benefit (CCB) If I File For Bankruptcy?

The short answer is no, you will not lose your Canada Child Benefit (CCB) if you decide to file personal bankruptcy. While your CCB will not be affected by bankruptcy, you are required to report your CCB when calculating and reporting your household income. These monthly reports will determine whether or not you have “surplus income”, which in turn will impact how long you are in bankruptcy and how much you will be required to pay.

Read MoreYour Credit Report After a Bankruptcy or Consumer Proposal

Debts included in a bankruptcy should be rated as R-9 or I-9, indicating written-off, and the outstanding balance should be reported as zero. There should also be a note indicating “included in bankruptcy” below the trade line for the corresponding creditor. Debts included in a consumer proposal should be rated as R-7 or I-7 and the outstanding balance should also be reported as zero.

Read MoreGuaranteed, Co-Signed and Joint Loans

Generally, a co-signor is usually jointly and severally liable for 100% of the debt. This means that, if there is a default, the lender will pursue the primary debtor and the co-signer at the same time and will be happy to collect their entire debt out of whomever they can recover from first.

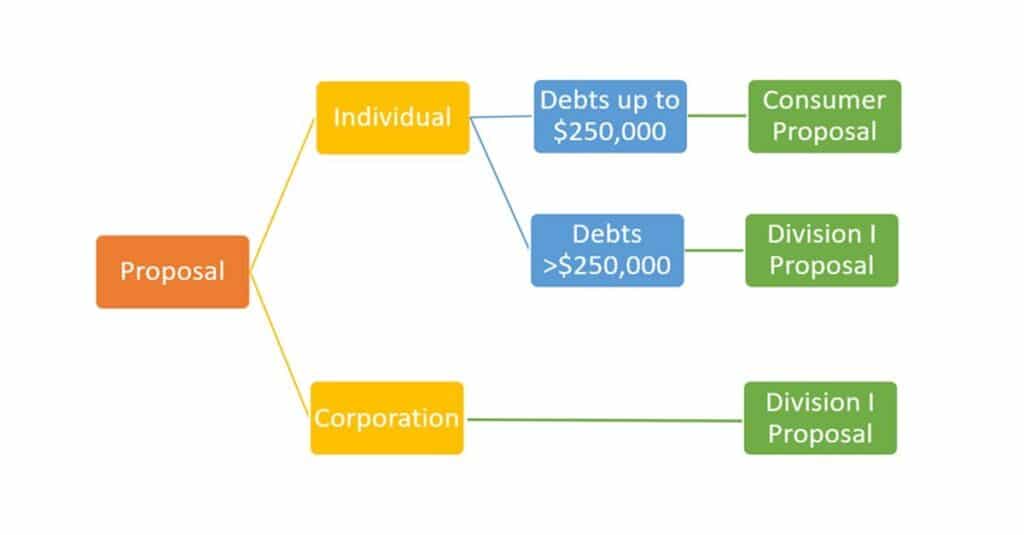

Read MoreDealing With Debt – Understanding the Two Types of Proposals

Division 1 Proposal Is when a consumer debtor owes more than $250,000 in debts, excluding the mortgage on their principal residence. If creditors don’t accept this proposal there is a deemed personal bankruptcy.

A consumer proposal is when a consumer debtor owes less than $250,000 in debts, excluding the mortgage on their principal residence. There is no deemed personal bankruptcy if the creditors reject the consumer proposal.

Read MoreWhat Happens If I Win The Lottery While Bankrupt?

If you win the lottery during your personal bankruptcy, before you are discharged, the lottery winnings are considered “after-acquired property” and forms part of your bankruptcy. After-acquired property can be seized by your Trustee in Bankruptcy for the benefit of your unsecured creditors.

Read MoreWhat Are My Duties In Bankruptcy?

There are several duties that an individual must complete as part of a personal bankruptcy to be eligible to be discharged from bankruptcy. These duties include, but are not limited to; completing two counselling sessions, report your monthly income to the Trustee, assist the Trustee with file your income tax return for the year of bankruptcy.

Read MoreWhat Is A Stay of Proceedings?

A stay of proceedings basically means that creditors must cease all collection or legal proceedings against the debtor, including wage garnishments. The purpose of the stay is to protect the assets of the bankrupt so the Trustee or Proposal Administrator can deal with them in an orderly fashion.

Read MoreBankruptcy And Sponsoring a Relative’s Application For Immigration

According to Immigration Canada, you can sponsor a relative’s immigration application as long as you are a citizen or permanent resident of Canada and are 18 years of age or older. There are however some restrictions, one of which states that you can not be an undischarged bankrupt.

Read More