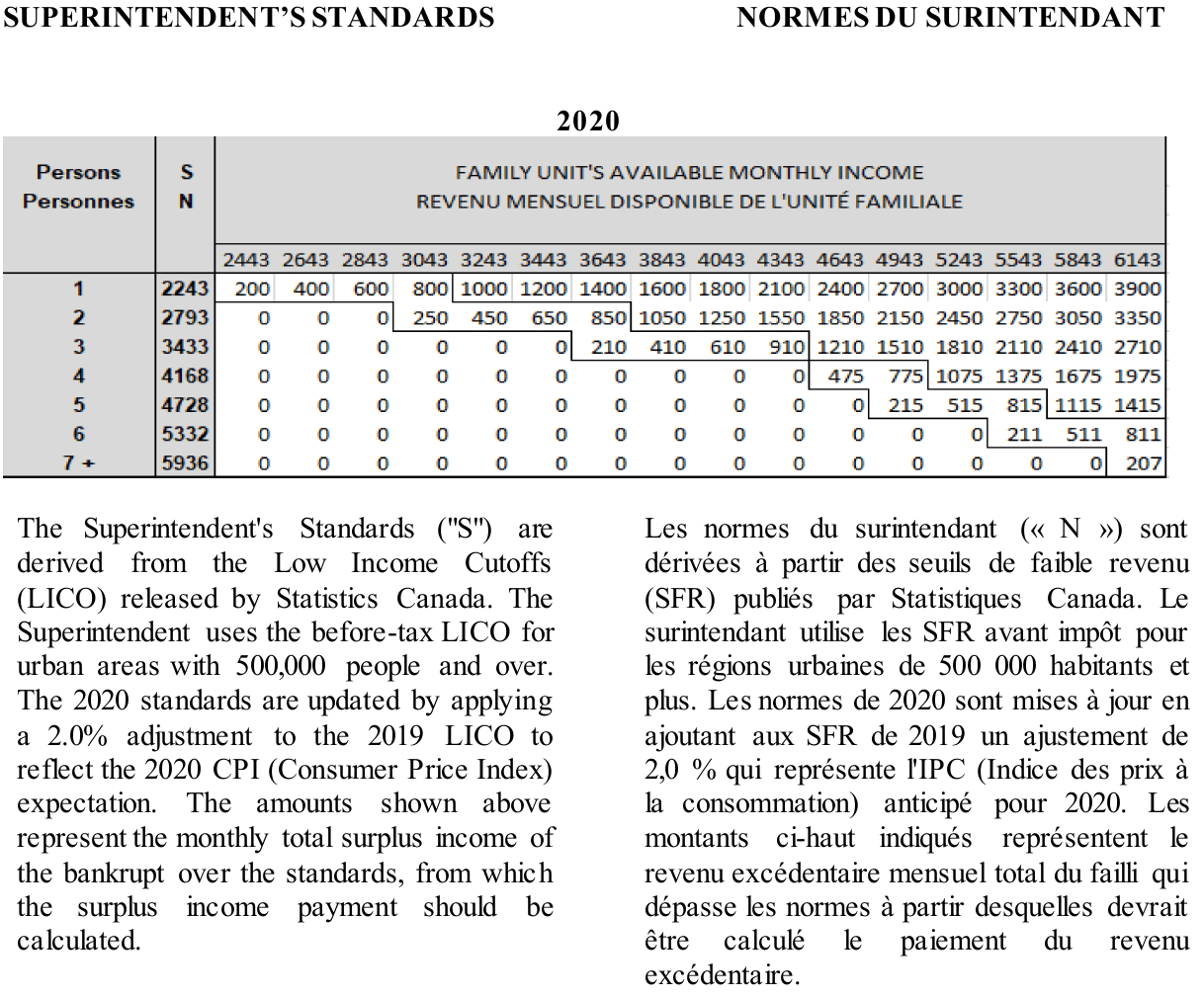

2020 Surplus Income Standards

On March 16, 2020, the Superintendent of Bankruptcy released the Superintendent’s Standards for the year 2020, used for calculating surplus income pursuant to Directive No. 11R2-2020.

{kind=link}

When an individual files a personal bankruptcy the trustee will calculate whether or not he will be required to make surplus income payments based on his net household income.

The Government of Canada has set net monthly income thresholds for a person or family to maintain a minimal standard of living in Canada. Every dollar that a bankrupt family makes above this level is subject to a surplus income payment of 50% while a person remains bankrupt.

Under the surplus income rules, the monthly surplus income payment is calculated using the following formula:

Net Income ( – ) government established threshold ( = ) surplus ( ÷ ) 2 ( = ) surplus income payment(Note: net income is calculated by subtracting any child/spousal support, child care or out-of-pocket medical expenses)

For example: John Dough lives alone and his take-home pay is $2,623 per month. Using the above formula, the monthly surplus income payment that he is required to make would be:

$2,623 – $2,243 (threshold for single person) = $380 ÷ 2 = $190

In this example, John Dough is required to pay $190 in surplus income payments for each month that he is bankrupt. He will be required to submit monthly income and expense reports to his bankruptcy trustee who will calculate his surplus income payment. If John’s pay increases, he will pay more and if his pay decreases, he will pay less.

If surplus income each month is greater than $200 (meaning that you are paying more than $100 each month in surplus income payments), a first-time bankruptcy is automatically extended to 21 months. Surplus income automatically extends a second bankruptcy to 36 months.

If this was John’s first bankruptcy he would be required to pay $190 for a period of 21 months. If John has a prior bankruptcy then he would have to make 36 payments of $190.

When surplus income payment requirements are high or if it’s a second bankruptcy, it might be more advantageous to file a consumer proposal. Our experienced team of insolvency professionals will review all of your options so you can make a decision that is best for you.

Powell Associates Ltd. is a Licensed Insolvency Trustee. We are experienced, hands-on insolvency practitioners who understand the personal impacts of major financial stress;

-

You won’t be stuck in an assembly line process.

-

You will expect and receive prompt responses and resolution of issues from our supportive and experienced team.

-

We will review your debt solution options, including filing a consumer proposal or personal bankruptcy.

-

We help Canadians with overwhelming debt get fresh financial starts.

Once you file a consumer proposal or personal bankruptcy, we deal directly with your creditors on your behalf. Your unsecured creditors are required to stop contacting you or continuing legal proceedings against you. Contact us for a free consultation.

We offer free consultations to review your financial situation and practical debt resolution options. Contact us to discuss your situation over the phone, a video chat, or in-person in Saint John, Moncton, Fredericton, Charlottetown, Dartmouth, or Miramichi.